Innovation in Member Loyalty Helps Credit Unions Remain Competitive

As PYMNTS.com introduced the Credit Union Innovation Playbook it developed in collaboration with PSCU, it stated boldly, “There is little mercy for those businesses that get loyalty wrong.” Based on our own experiences as marketers with expertise in credit card rewards programs and financial services customer experience, we have to agree. The upside of that hard, cold fact, however, is an opportunity. As it says in the Playbook, “Many credit unions have an opportunity to use innovation to improve member relationships going forward.”

According to the PYMNTS.com and PSCU report, nearly 50% of credit union members list “loyalty/rewards” as the number one innovation priority for their FI, even ahead of “account fraud/theft protection,” “data security” and “special offers.” In contrast, less than 30% of credit union decision-makers say their CU has focused on loyalty innovation during the past three years, far behind “fraud management,” “real-time payments,” “digital wallets” and other initiatives.

The stats in the Playbook paint this picture: customers want innovation in credit union member loyalty and rewards, but most credit unions are not prioritizing these programs. Beyond an ability to meet customer expectations, there are many reasons CUs should change this right now and give loyalty and rewards more attention:

- As identified by Salesforce, customer loyalty programs lead to “better customer retention, more customer referrals, cost efficiency and user-generated content” (specifically content that boosts a brand’s reputation, like reviews, ratings and social media posts).

- Experts cited by Credit Union Journal say that rewards programs “keep your members engaged. They give you more touch points with your member and forge a lasting relationship.” In addition they say these loyalty initiatives are an “imperative for them to remain competitive in the market.”

- Rewards can also help CUs reach business goals. As reported by the St. Louis Business Journal, the Anheuser-Busch Employees’ Credit Union used cashback rewards to boost mortgage loans 187%.

So what would innovation in credit union member loyalty and rewards look like? Here are some guiding principles and thought starters:

Think beyond transactions.

We love what Credit Union Journal shares from CU Engage’s Jennifer Addabbo. She says, “By providing a holistic-level loyalty program, credit unions can compete with card issuers who only have a single credit card relationship with the consumer. They should be thinking about things like buying down loan rates or buying up CD rates, having a shorter call queue for members who have deeper relationships with them with multiple products [and] taking into account the ability to spread the expense of a loyalty solution across the entire enterprise, instead of just using it to drive up transactional volume and taking the expense against the card program.”

Enroll members automatically.

NASA Federal Credit Union enrolls members in its reward program automatically, and the benefit is two-fold: it shows you care about every relationship right from the beginning, and it provides members with added benefits beginning the moment they choose your FI.

Reward family loyalty.

Madison Credit Union’s “Household Feature” encourages relationships with everyone in the member’s family by extending the highest rewards level in each household to other members at that same address.

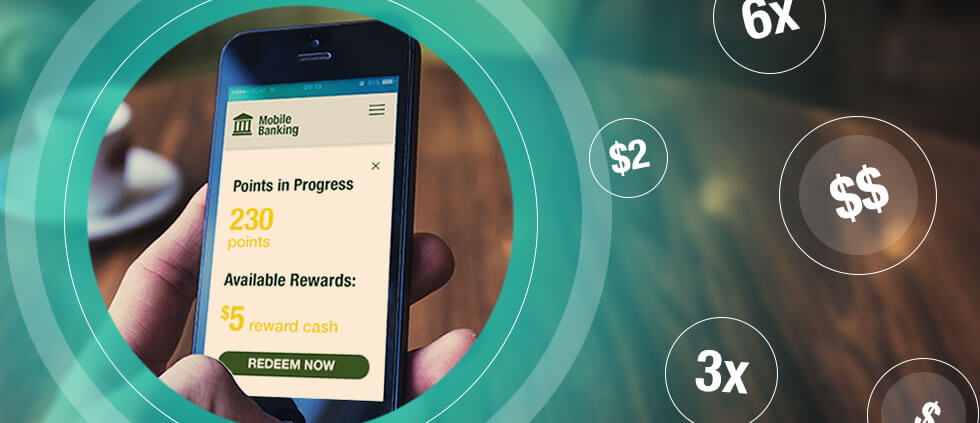

Leverage data to personalize and improve the member experience.

As Salesforce points out, “Customer loyalty programs aren’t just about offering discounts. They use the purchase history and customer-provided data to present customers with timely and relevant offers; and they improve overall customer experience. Companies can also grow their customer base and deliver even more compelling rewards by forming innovative partnerships with related businesses.”

Consider accelerated timelines for distributing rewards.

Cutting back the time members need to wait for rewards may increase engagement and enthusiasm. For example, Texas Trust Credit Union members with Bonus Checking accounts qualify for monthly cash rewards. This offers an important – and frequent – opportunity for the credit union to nurture relationships with members.

Create partnerships that boost rewards.

Navy Federal’s Member Deals are extremely competitive: up to 15X the points or up to 15% cash back per dollar spent. (Note that Navy Fed’s drive to offer industry-leading rewards extends to its credit card products; last month, the CU announced its More Rewards American Express Card now offers 3X points on dining and transit. The card already offered this points level for purchases at supermarkets and gas stations.)

Tie your rewards program to something meaningful.

To celebrate its 85th anniversary, PSECU announced the largest reward it had ever returned to members: “$22 million in surplus earnings in honor of our 22 founders.” And then it showed how the funds would be distributed, including, for starters, a $22 reward to all eligible members.

To encourage members to shop local and keep local dollars in the community, Shoreline Hometown Credit Union’s rewards program issues gift certificates specifically for participating Hometown small businesses. Texas Trust Credit Union helps members earn cash for their local schools (most recently, the amount donated topped $500K).

Play to your strengths to compete with larger FIs.

The Financial Brand says that, although large issuers have “access to the latest tools, technology and investment dollars,” community banks and credit unions often know more about the timing of customers’ key life events and the relevance of particular bonuses. They benefit from frequent interaction across multiple channels and the ability to be faster – and more nimble and creative – with rewards.

Use rewards to alleviate member pain points.

There are several times a year when members are likely spend more than normal, which can strain budgets and increase debt. Neighbors Credit Union helped its members get a little relief during one recent high-spending season: back to school.

Don’t forget about debit.

Calling credit unions’ failure to optimize debit card portfolios a “missed opportunity,” Credit Union Times says there are a number of ways CUs can incentivize debit card utilization, including awarding gift cards or bonuses based on transaction volume or rebates for making the CU’s credit or debit card the card-on-file (COF) for specific services.

Takeaway

Even though so many members rank loyalty/rewards as #1, FIs are going to continue to prioritize fraud management and real-time payments above credit union member loyalty and rewards programs: they can’t afford not to. However, credit unions still need to invest in getting rewards up to the top of the list, not at the sacrifice of something else that is critical, like data security, but in addition.