Consumer Frustration with High Deductibles Prompts Some Health Insurers to Offer New Types of Plans

Flashback to 2014 when millions of Americans received healthcare coverage under the Affordable Care Act (ACA), many for the first time ever. The ACA precipitated a major shift to employer sponsored health plans with higher deductibles and many saw consumer out-of-pocket costs rise. Fast-forward to present day and it’s abundantly clear, as stated in a 2018 Deft Research 2018 Employee Choice and Preference Study, that “carriers know that the word “deductible” is the most hated health insurance term,” especially because “most consumers have a high deductible today, and the amount of their deductible has risen sharply in the last three years.”

With higher out-of-pocket minimums, the logic behind high deductibles is to create awareness of medical costs which in turn, causes members to think more critically about healthcare spending. The concept of the “empowered healthcare consumer” emerged alongside high deductibles, but also the false assumption that people were prepared to navigate narrow providers networks, deductibles, coinsurance, formularies, HSAs, FSAs, and the list goes on.

In reality, there are major obstacles prohibiting consumers from making cost informed decisions, the most notable being a widespread lack of health literacy. An Alegeus survey reported that more than 50% of participants failed the health insurance fluency test, 51% of consumers struggled to understand the pros and cons of each plan and 50% didn’t understand what services would count against their deductibles. Out of those surveyed who “claimed confidence, half still answered simple questions incorrectly.” Furthermore, members often struggle using tools like cost calculators and adequate educational support can be hard to come by. The result? Patients may receive an unexpected (and expensive) bill after services which not surprisingly, reduces satisfaction with their plan.

Barriers have left consumers frustrated with high deductibles, and many remain ill-equipped to advocate for themselves in the marketplace. A number of startups are responding with the “what’s old is new again” approach and testing health plans without deductibles, a concept that could better meet the needs of today’s consumers.

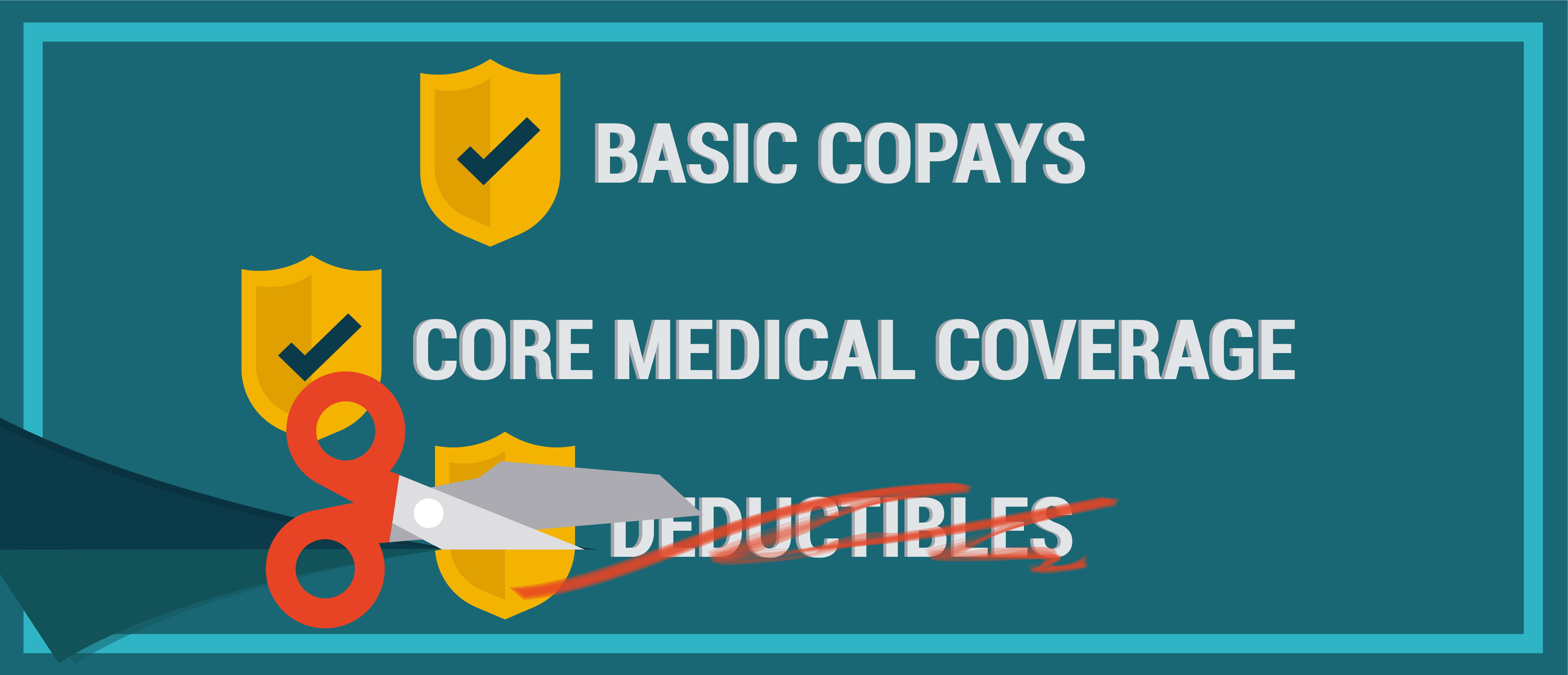

Shelby Livingston of Modern Healthcare recently spotlighted startup Bind Benefits, a health insurance provider that thinks deductibles hinder people from receiving proper healthcare. Their “core coverage” lowers premiums by removing unnecessary benefits and the total cost of care is available well in advance of services rendered. On-demand “Add-Ins,” “paid for via additional copays and paycheck contributions,” can cover expenses that arise outside of the standard offering. Dove Healthcare, a nursing facility in Wisconsin, has contracted with Bind in order to give their 500 full-time employees “lower premiums and straightforward copayments.”

Centivo is a self-proclaimed “new type of self-funded health plan” that removed “confusing high deductibles that keep people from getting the care they need.” Their focus is on connecting patients with quality primary care providers to not only improve health outcomes, but also control cost. An innovative primary care-centered network, dynamic benefits design and an advanced technology platform with concierge support are all readily available tools for members.

According to the 2018 Oliver Wyman Consumer Survey of Healthcare, “today’s insurance products are out of sync with consumer wishes.” We don’t anticipate this means employers will abandon plans with high deductibles completely and based on findings from the 2018 Deft research, there could be opportunity to sooth member frustration. The study revealed that if premiums remained the same, participants were willing to forgo out-of-network coverage in favor of a reduction in their deductible. Most importantly, this option doubled plan satisfaction among those surveyed. On the other hand, startups like Bind and Centivo are appealing to consumer aversion with an approach that directly alleviates many of the sore spots found with high deductibles. The healthcare marketplace is in a state of flux as new solutions emerge and employers are reassessing plans with high deductibles, leaving us eager to see the evolution of product development in 2019.