Financial Services Marketers Can’t Ignore Elevated Consumer Expectations

Customer disappointment is jeopardizing banks’ business models. That’s a paraphrase of the bold statement that opened an American Banker article recently.

In the article, “Banks’ New Digital Battlefront: The Customer Experience,” Mary Wisniewski quotes Jim Smith from Wells Fargo:

“Customer expectations are shifting dramatically. They are not being shaped by peer-competitor banks. They are being shaped by Apple. They are being shaped by Google. They are being shaped by Amazon. Too often, as an industry, we’re not living up to expectations.”

Jeff Dennes from BBVA Compass agrees. In June, he told attendees at a banking summit that financial services consumers “continue to have underwhelming banking interactions.”

Simultaneously, customers have been experiencing the convenience of self-service in many industries and gaining 24/7 access in others. Uber, and companies like Apple, Google and Amazon (as mentioned by Smith), are changing the way consumers interact with companies. It’s on their time. It’s very often on mobile devices. It’s nearly always easy, intuitive and satisfying.

In short, these companies have ratcheted up consumer expectations. And now even more complex industries, such as financial services, are being held to the same standards.

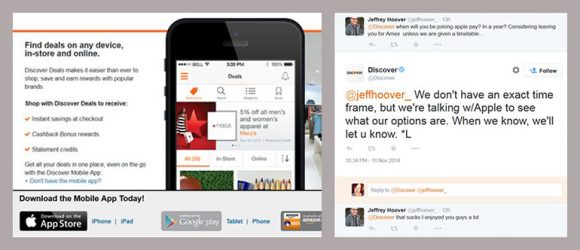

And we’re already seeing its impact, of course. According to the Federal Reserve, 52 percent of bank customers with smartphones use mobile banking. Banking apps are among the most popular applications, says MediaPost. Bank of America has reported that 12% of its deposit transactions occurred via mobile in Q4 (2014). JPMorgan Chase has more than 20 million active mobile users. And, says Digital Trends, every major credit card company in the U.S. has Apple Pay support, which works at 700,000 locations.

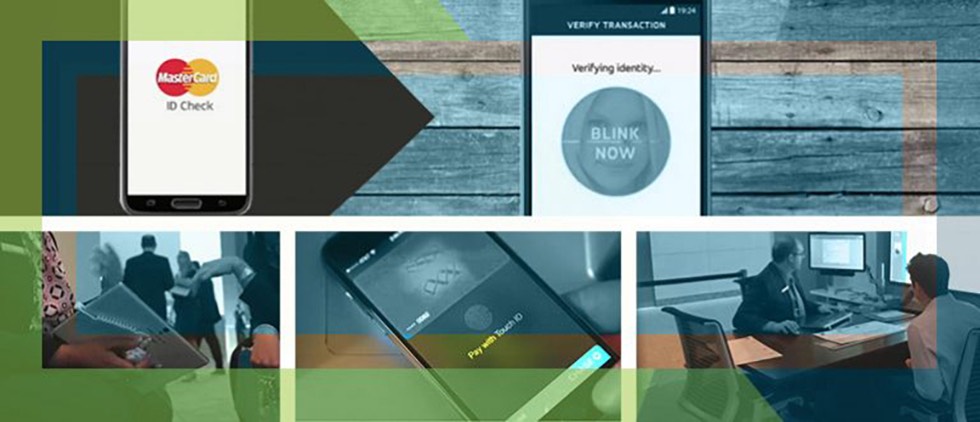

As consumers are saying “yes” to exciting new technologies and “no” to “underwhelming banking interactions,” it’s clear that banks and credit card issuers must stay on top of their customer experiences. As detailed in the American Banker article, many are doing just that. Customer identification and verification is evolving, for example, with Mastercard testing facial recognition for purchases and USAA permitting voice and facial recognition for mobile app access. Banks are re-evaluating customer service and attempting to be more relevant and engaging by offering location-based discounts and information.

However it manifests, digitally, in-branch or both (check out this “bank branch of the future” video from Chase), the bottom line is that customer expectations are making a lot of the rules. And so marketing – through its contributions to product design, acquisition and customer relationships – must emphasize those qualities and conveniences consumers are finding most desirable. Of course, it’s always been that way, right? Financial services marketers have always been adept at finding the right message.

The most poignant difference – and challenge – now may be that it’s no longer enough to be good and trustworthy at what you do: payments, lending, etc. Because consumers are nurtured so skillfully by other industries (those that are very high-tech and purchase/service-driven), financial services customers understand what’s possible. That means they depend upon brands to be always “on” (not just 24/7 but glitch-free), always relevant (not just in the moment but also predictive) and always helpful.

If that kind of precision customer focus isn’t yet part of your business model, then you may want to consider this caution from U.S. Bank’s Niti Badarinath as quoted in the American Banker article: “We are trying to disrupt ourselves before we get disrupted. We are all concerned about an Uber of banking.”

However, in this world of satisfying multiple expectations, in real time, with customers who assume they can experience the highest level of interactions from all brands, we find our bank clients sometimes overlook the obvious in the stories they can tell. Case in point: Many banks failed to encourage cardholders to set up their branded card as the default Apple Pay payment. That key step could have helped them own the payment disruption. And here’s one more example: As EMV cards are being mailed in mass updates of the old plastic, brands that fail to hype the benefits they provide – defaulting to basic “we have replaced your card” messaging – are missing an opportunity.

We see these kinds of misses too often in financial services marketing. Sometimes, the chance to creating a sense of belonging to – and being part of – the disruption slips right out of marketers’ hands.