Rethinking How Credit Products Can Better Connect With Customers

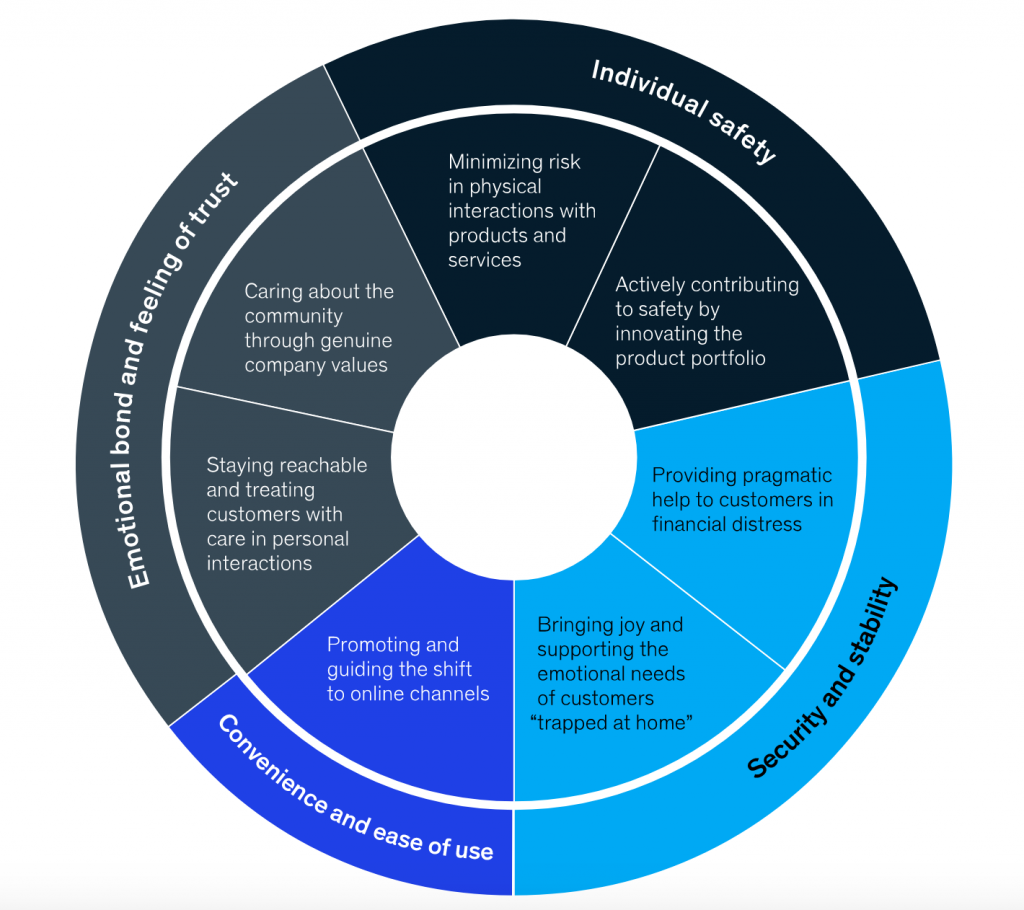

Earlier this year, McKinsey & Company advised brands on how to rethink their products and better connect with customers during the current environment and into the future. In its guidance, McKinsey articulates four core consumer needs – individual safety, security and stability, emotional bond/feeling of trust, convenience and ease of use – and notes multiple actions laddering up to each need.

In repositioning credit products, it appears that banks, payment issuers and fintechs made the jump quickly from pitching “wouldn’t it be nice” to offering real world solutions for these unprecedented times. Tapping into marketing examples captured by Comperemedia*, we looked at how financial brands are repositioning credit products right now and found approaches ranging from credit product tweaks to product invention/repositioning.

Core Need: Security and stability

Recently, as reported by McKinsey, banks and issuers have waived fees and interest charges either upon request or as a general policy. Goldman Sachs allowed Apple Card users to skip March payments. Ally Financial allowed auto loan and mortgage customers to delay payments.

In the meantime, some brands have been hard at work inventing new ways (or promoting alternative paths) to access and use credit.

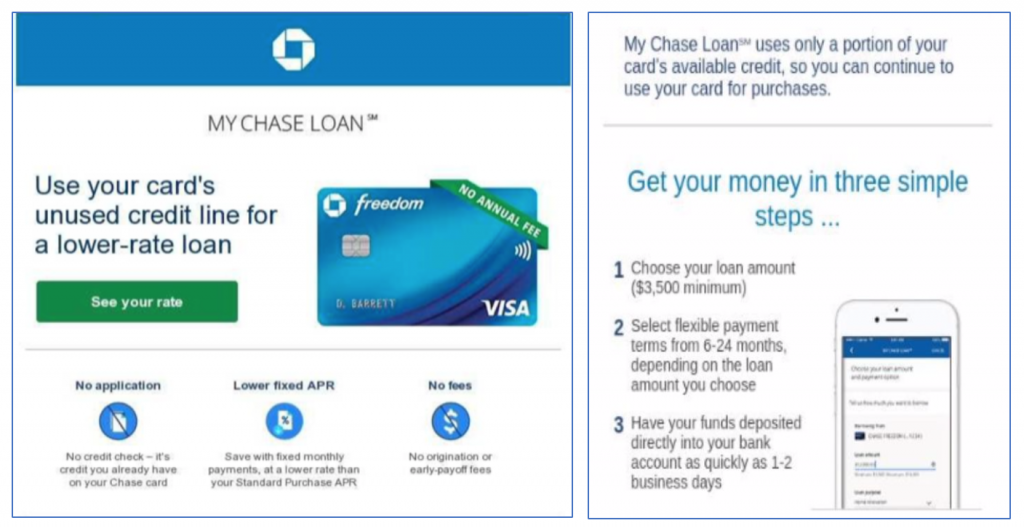

For example, Chase is turning open lines of credit (LOC) attached to credit cards into Chase loans. Chase credit cardholders receive communications allowing them to choose their loan amount from their open card LOC to gain both flexible payment terms and a low rate. Application is quick, and the rate is personalized to the cardholder who converts to a My Chase Loan.

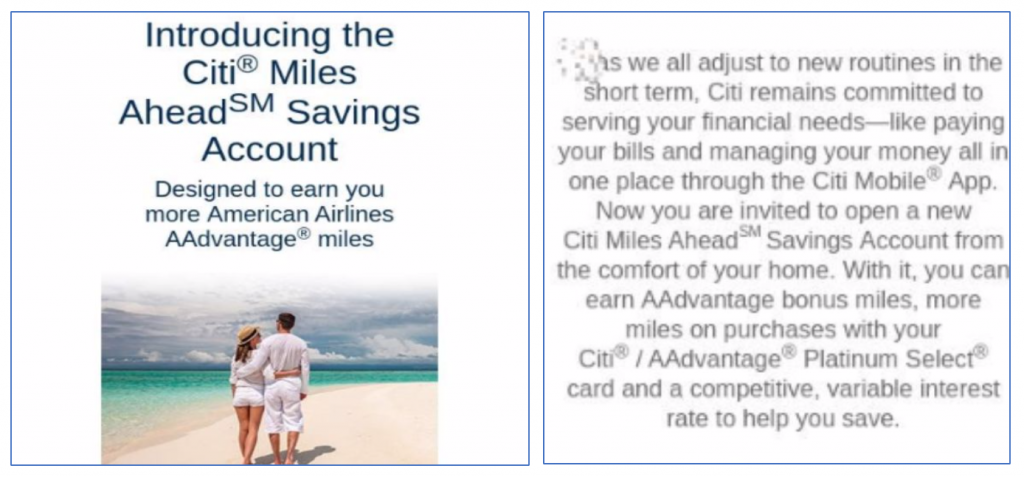

Citi introduced Citi Miles Ahead Savings, a new digital savings account targeting cardholders who do not live within proximity of a physical branch. This cross-sell promotes competitive rates and a bonus miles offer of up to 50K miles for meeting the top tier savings deposit requirement. Savings accelerates earning miles as the enrolled cardholder also earns 25% more miles on everyday purchases.

Core Need: Convenience and ease of use

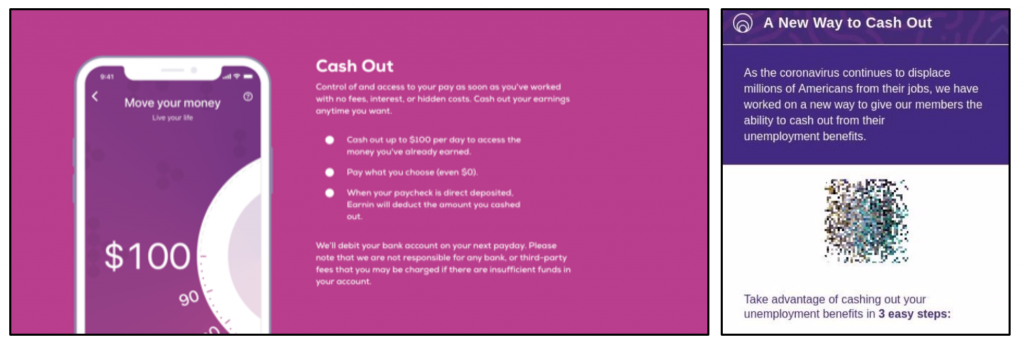

In its recent “Positioning Credit to Consumers” report, Mintel took note of how disruptors rose to the challenge and offered simple financial solutions to struggling consumers, such as cash advance applications to access funds quickly.

Fintech Earnin, for example, introduced and promoted “a new way to cash out” and tap unemployment benefits early using the cash advance app. The program helps consumers avoid payday loans and their high interest rates, although the payback terms may prove to be too short given the consumer’s inability to quickly change their unemployment or furloughed status.

Core Need: Emotional bond and feelings of trust

Skeptics may say an emotional bond seems a far-fetched expectation of a financial brand, but many credit providers are successfully promoting and messaging credit solutions based upon the “actions” McKinsey suggests to meet this consumer need. These include demonstrating caring about the community, staying reachable and treating customers with care.

Citi, at the brand level and in communications directed at credit cardholders and with an emphasis on mobile app capabilities, consistently messages ways to easily and conveniently reach help. These communications also remind cardholders about valuable content available to solve problems. The insert shown below, for example, puts a human spin on digital assistance by featuring Customer Service Reps who are easy to engage and ready to handle common credit problems and needs.

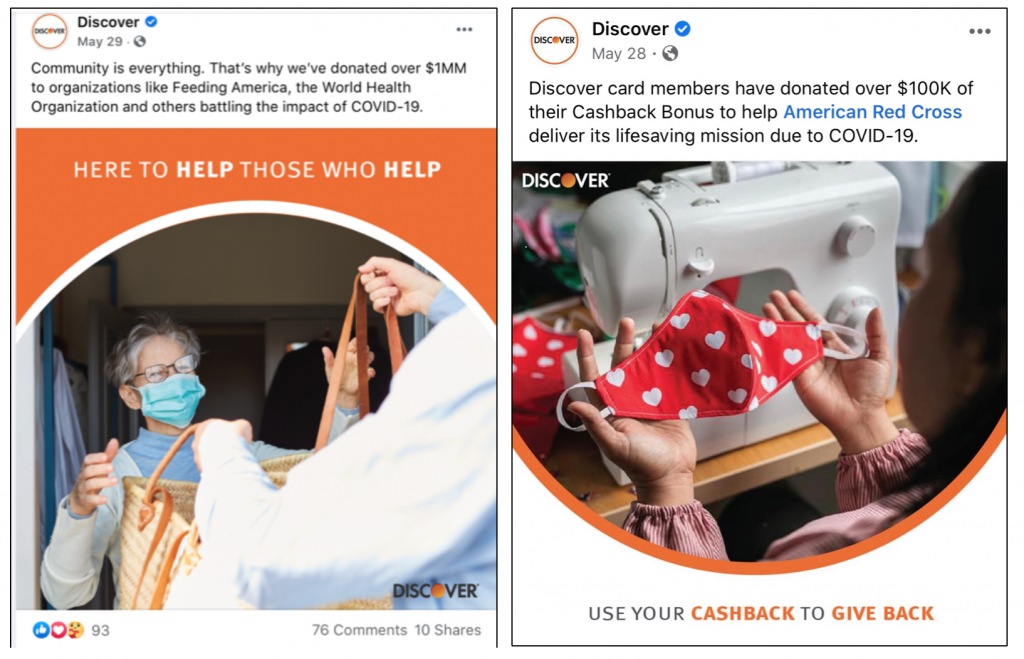

There are also countless examples of brands supporting community needs during the pandemic. Discover, for example, uses social media to raise awareness of both cardholder giving (use of earned cash to support COVID-19 related needs), as well as the brand’s corporate-level support.

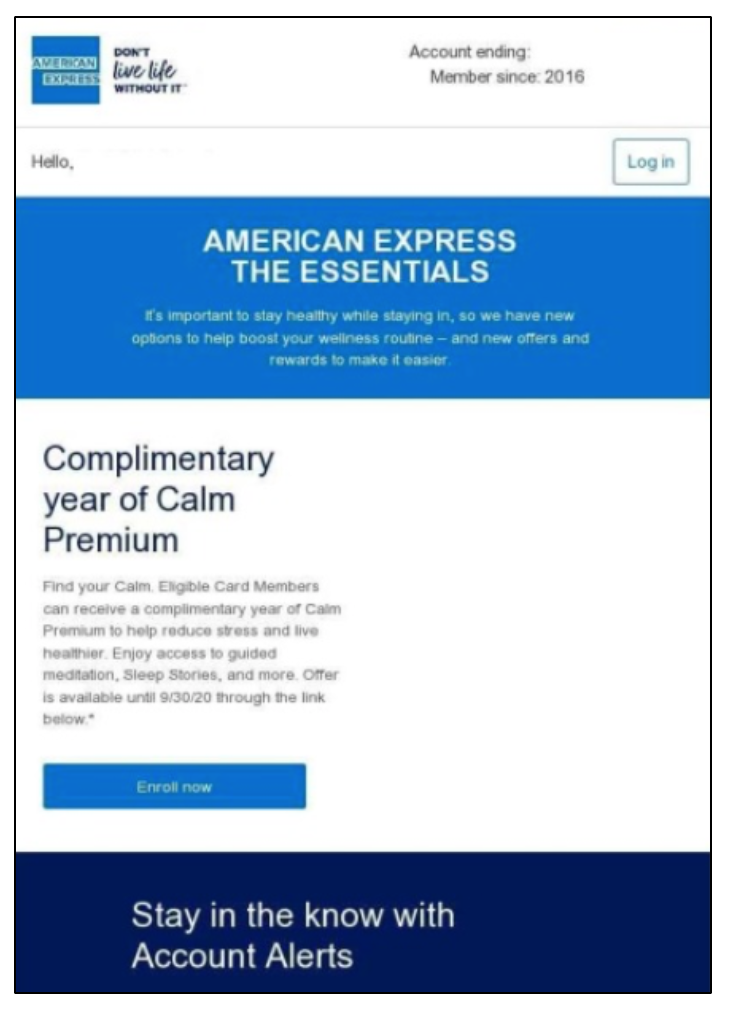

Recognizing consumers’ feelings of anxiety and uncertainty, Amex offered eligible cardholders a complimentary year of Calm Premium to support health and well-being through meditation, sleep stories and other resources.

Looking at this financial brand activity as a whole, we agree with Mintel’s recent observation:

“Brands have a unique opportunity to position their products in new ways to attract customers… Brands should focus more heavily on building loyalty through opportunities provided to current customers.”

Repositioning credit products, while keeping the McKinsey consumer core needs as guidelines, will deliver a win for consumers and a win for brands during the next normal.

*Source: Mintel. Positioning Credit to Consumers. May 2020. All marketing examples (except those from websites or social media) are sourced from Comperemedia.