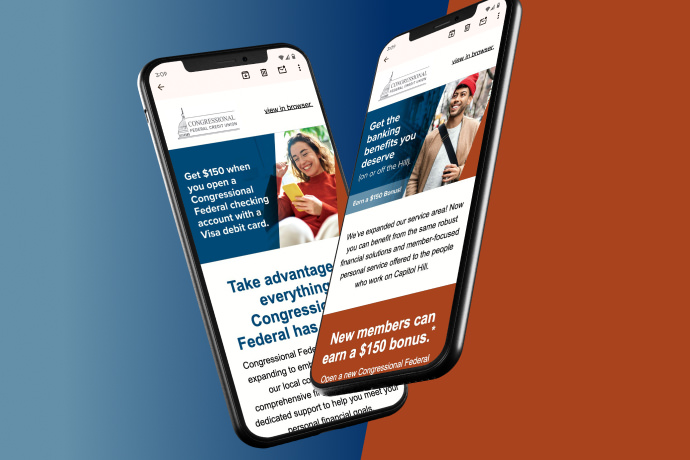

How Credit Unions Can Seize Buy Now Pay Later Opportunities

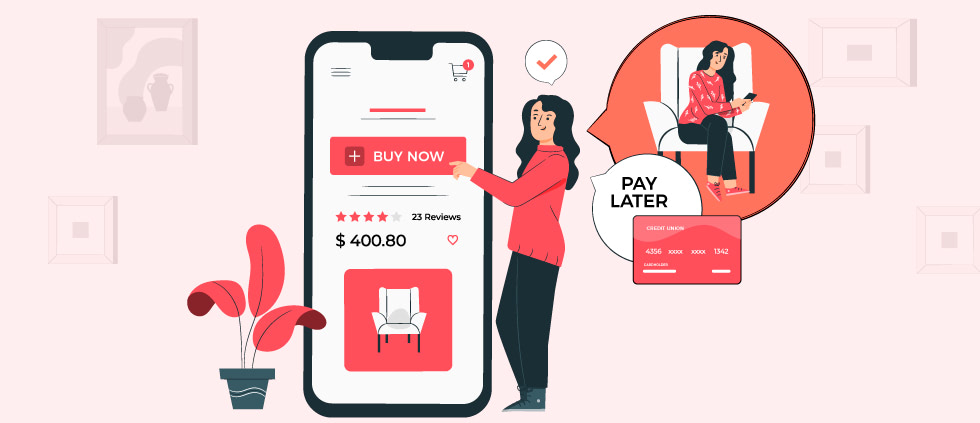

As Buy Now Pay Later (BNPL) continues to boom, more financial institutions are taking aim at the feature. To support this, Payment Systems for Credit Unions (PSCU) recently launched a solution that will allow the roughly 2,400 credit unions they serve to provide BNPL options.

According to PYMNTS, this program offers credit card customers a “flexible payment method that helps them budget and plan for larger purchases” by enabling some post-purchase card transactions to be converted into installment payments. PSCU says its solution is unique from others because it uses existing lines of credit.

PSCU Managing Vice President, Payments, Fraud and Loyalty Cody Banks says that this benefit may help credit unions promote their credit card as the card of choice for customers with an interest in BNPL. Ultimately, he says, this may boost interchange revenue, deposit balances and brand visibility.

Currently, BNPL accounts for 3.8% of e-commerce sales in the U.S. and an even higher rate of almost 10% in Europe.

As credit unions seek to take advantage of this growing opportunity, we recommend keeping the following BNPL marketing best practices in mind.

Focus on your existing customer relationships.

Research shows that some consumers opt for point-of-sale BNPL over using a credit card because they believe it’s the more financially responsible option. It’s important for credit unions to reframe this idea: Remind your customers that using a card-associated installment plan within an existing credit line is the wiser and more strategic move. This can also be a great chance to highlight the peace of mind that accompanies working with an established financial partner.

Rethink your target audience.

Scrap whatever you’re picturing as your target BNPL customer. Research indicates that BNPL actually attracts a diverse customer base that extends across ages and income levels.

Strike while the iron is hot.

Take advantage of key moments to promote BNPL. For example, highlight them in onboarding communications and promote them again when your customer makes a major purchase. If and when your customer does choose to use your BNPL offering, send a confirmation email with the payment plan and timeline to validate their decision by helping them feel organized, informed and in control.

Keep it simple.

In our analysis of how major credit card brands market their BNPL features, we’ve seen an emphasis on convenience and simplicity. Make it clear how users can access the payment option and ensure the process is straightforward. (We’ve seen previous BNPL offerings fall flat due to complexity.)

We’re eager to see how this payment option continues to gain traction in credit union card portfolios and will continue to monitor the space, including how FIs may choose to address the regulatory and financial wellness challenges associated with BNPL.