Trends in Credit Card Acquisition

Prefer to Listen? Hear directly from Media Logic’s Financial Services team on the latest credit card acquisition trends and the implications for FS marketers:

Fact: The U.S. adult population grew by 10% from 2016 to 2025 while credit card acquisitions grew at a rate almost 5x faster. While consumers and businesses are accumulating credit cards, cardholders are increasing debt, by more than $360B across that timeframe (Javelin Strategy).

Bank of America provides a lens into potential growth of the category as BAC has set an ambitious goal of growing their customer base – including their card business – from 69 million to 75 million in four years while significantly also expanding their Preferred Rewards membership which includes cardholders (Payments Journal).

Behind the credit card growth are strategies ranging from the tried and true to emerging trends in successfully acquiring cardholders and attracting new audiences.

Targeting a bifurcated prospect universe

Recently, we have witnessed a major push in pursuit of premium cardmembers fueled by product refreshes from Amex, Chase, and Citi with annual fees reaching $895 (Emarketer).

At the same time, FIs are also addressing lower and middle-income consumers who face tighter credit access. Generational shifts – focused on Gen Z – impacts product design and marketing of low interest rates versus rewards as Gen Z largely searches for a credit card based on rate messaging.

To attract the younger audiences seeking their first credit card relationship, FIs are also investing in creator partnerships to generate financial education content on TikTok and YouTube while creating brand awareness and engagement amongst novice cardholders.

Payments Journal advises FIs with aging customers and cardholders how to ensure they, “have business for decades to come.” This advice focuses on what they call the big trio: digital wallets, BNPL and contactless. These are considered high-growth areas with appeal to desirable younger cohorts seeking a credit card.

To that end, acquisition communications must emphasize digital features and – in an ideal world – immediate digital card delivery immediately upon approval. This drives activation ahead of plastic delivery and results in earlier card utilization, an Early-Month-on-Book best practice.

Fulfilling prospect expectations: Value versus rising annual fees

As big brand players seek to capture and engage the Gen Z affluent segment, the premium cards referenced earlier are enhanced with new benefits, perks and, of course, higher annual fees. Successful FIs understand the “quid pro quo” in play. In fact, Auriemma Group research has validated that “Expectations climb steeply with the annual fee. Perks and benefits are the leading driver of acquisition, and cardholders expect them to scale with cost. For a card like the Chase Sapphire Reserve, that translates into a substantial value threshold: 25% of annual fee cardholders say it would need to provide $5,000 or more in value to justify its $795 price tag.” (Auriemma Group)

Exponentially rewarding multi-product relationships including card

Banks are now offering tailored incentives to customers – including cardholders – with higher account balances. According to Payments Journal, Bank of America has just announced a shift to expand their positioning of the credit card as a comprehensive tool for customer management. The total banking relationship – including BAC card ownership – will earn more rewards complete with built-in reward accelerators.

A new, expanded BofA Personalized Rewards program will launch in May 2026, and will lower the entry barrier to include all checking account holders to “bring you personalized benefits, moments of delight and more ways to get the most from your relationship.” BAC touts that “more than 30 Million clients are newly qualify for Personalized Rewards” with cardmembers in the mix.

Using lifetime value to amortize acquisition costs especially big intro offers

FIs continue to leverage enhanced offers and introductory benefits as they are attractive to potential cardholders. In fact, a recent survey shows weak sign-up offers can have a detrimental impact on likelihood to apply – even attractive rewards cannot make up for a weak offer.

An accounting strategy is playing out with a focus on high-end credit cards and reward cards. To support these powerful front-loaded offers, FIs turn to amortizing the cost of these incentives over the anticipated lifetime value of the new cardmember – an accounting technique referred to as “cost spreading.”

Instead of recording a large, one-time marketing expense, issuers use amortization to spread acquisition costs over an estimated 84-month customer lifetime, transforming a $1,000 cost into a $12 monthly expense. Issuers are clearly betting on earning long-term revenue from interest and fees after the promotional period ends (Payments Journal).

Leveraging third-party comparison environments

Consumers shopping for a new credit card will routinely compare their options – from rewards versus cash back and intro offers to evergreen benefits, annual fees and eligibility requirements. As such, credit cards are uniquely reliant on third-party comparison environments and brands must show up consistently in the places where consumers evaluate their options.

Fintel Connect points out that consumers now ask very direct questions and AI tools and large language models (LLMs) can answer immediately using a handful of trusted sources. This concentrates attention around publishers and card comparison sites for answers. LLMs generate answers that rely heavily on external sources to arrive at recommendations.

“AI is rewriting the rules of financial discovery. Consumers aren’t clicking through search results – they’re asking LLMs like ChatGPT and Gemini for answers. And who gets cited matters more than ever.” – Fintel Connect

SEO may no longer be enough. Now, affiliates and publishers are “the gateway to visibility, appearing in 70-74% of AI-cited financial recommendations and shaping which brands show up, earn trust, and influence decisions”. Your card acquisition objective should be to be seen where AI looks (Fintel Connect).

Using AI to manage risk and expand the credit-worthy segment

FIs are implementing faster and smarter approvals by using multiple data sources, specialized agents and adaptive models. The benefits are speed and reduced costs. AI helps issuers incorporate “non-traditional signals while actively monitoring for bias” to better serve the underserved. Potential cardholders are screened with more efficiency and potentially greater satisfaction while meeting regulatory compliance (Banking Exchange).

As previously noted, Bank of America has ambitious goals for growing its customer base – from 69 million to 75 million in four years – and their stated strategy will deploy AI to refine customer acquisition across all products including credit cards while also using AI to improve credit risk decisions.

Using AI to enhance ubiquitous direct mail

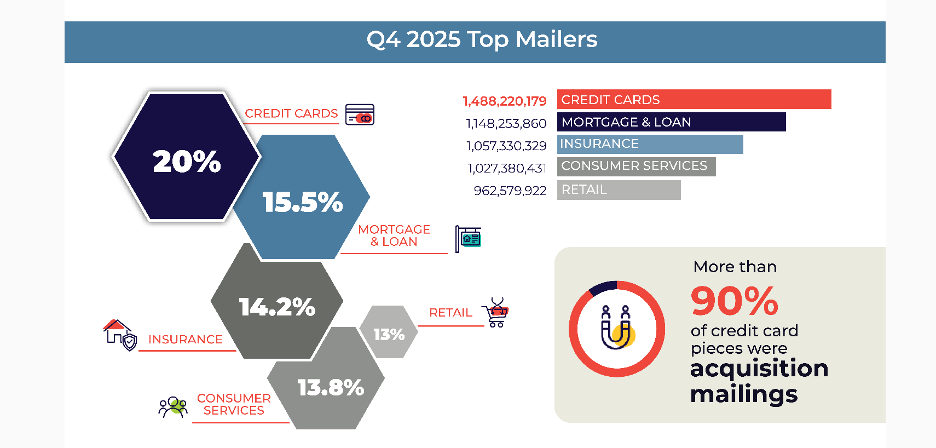

Q4 2025 mail volume indicates mail remains a card acquisition workhorse…with 90% of the 1.5B credit card mail categorized as acquisition mailings. How can FIs stand-out and optimize mail in this highly competitive channel?

AI can transform direct mail campaigns in several ways with precision targeting to reducing waste, lowering CPA and increasing ROI. Successful FI campaigns are using AI tools for personalization at scale resulting in more engaging and responsive outreach. AI advanced tracking provides analytics in real time. The takeaway: the future of direct mail marketing lies in automation, predictive modeling, and measurable optimization enhanced through AI.

“Precision now defines winning marketing strategies. Modern direct mail no longer depends on static lists. It integrates artificial intelligence, behavioral modeling, predictive analytics, and automated workflows to determine who receives mail, when they receive it, and what format will generate the highest response. The result is stronger direct mail performance, lower waste, and dramatically improved ROI across sophisticated direct mail campaigns.” – SSIcards