Are Cashback Cards Getting Back to Basics?

When you think about it, the whole point of a cashback rewards card is simplicity: no points or miles to track, no catalogs to peruse, no blackout dates to consider. You spend on the card, and you get a percentage back as cold, hard cash (a.k.a. a statement credit).

And yet, for years, we have watched issuers try to reinvent or evolve the cashback space with different offerings. For example:

- Rotating category bonuses / Discover, one of the leaders in the cashback space, focuses most of its card marketing on Discover it, which gives cardholders 5% back on spend categories that rotate quarterly (right now it’s for gas stations, ground transportation and wholesale club purchases) and 1% on all other purchases. Chase Freedom offers 5% back on rotating categories (currently gas and transportation), as well, and promotes it with strong product positioning: “The card is for the essentials, the cashback is for the fun.” Not to be outdone, U.S. Bank’s Cash+ card follows this rotating category bonus approach; it has both 5% and 2% bonuses, and cardholders pick the categories each quarter.

- Tiered earn / Some issuers take a similar approach, but skip the rotating categories. Bank of America offers the BankAmericard Cash Rewards card with 1% back on all purchases, 2% for grocery stores and wholesale clubs and 3% on gas. The American Express Blue Cash Everyday card offers 3% back at supermarkets, 2% back at gas stations and “select” department stores and 1% on everything else.

- The outlier / Of course, we can’t overlook the Citi Double Cash card, which gives cardholders 1% back when they use the card and another 1% back when they pay off purchases. Citi launched this card in 2014, and so far, no other issuer has attempted to replicate this value prop. Citi clearly ties the product name to its unique earn structure.

What’s the point of these different approaches to cash back? They help issuers position their products in ways that set them apart. Rotating categories offer “choice” and put the customer in control. Fixed bonuses award spend on “everyday purchases,” offering an alternative to debit cards: you’re going to buy gas anyway, why not get something out of it?

But there is a catch, most of these bonus categories come with an earning cap, and once you hit that, there is no more bonus. So, in addition to tracking spend categories, cardholders may also need to track how much they spend to know how much they will earn.

So much for simplicity.

Or maybe not. Recently, we’ve taken note of several cashback cards that seem to be re-embracing the simple approach. These generally have a flat earn, but importantly remove the cap. Here are a few that seem to be getting back to basics:

- Capital One was among the first to offer a flat, unlimited 1.5% cashback earn with its Quicksilver Card. It’s worth noting that Capital One’s lead message online plays up both the unlimited earn and the idea of “every day” purchases.

- Chase has evolved its product offering, and it now promotes the Freedom Unlimited credit card as its lead cashback card. It also offers 1.5% back with no cap. Here’s an interesting line of copy from its landing page: “Earn unlimited 1.5% cash back on every purchase – it’s automatic.” (You don’t have to pick a category.)

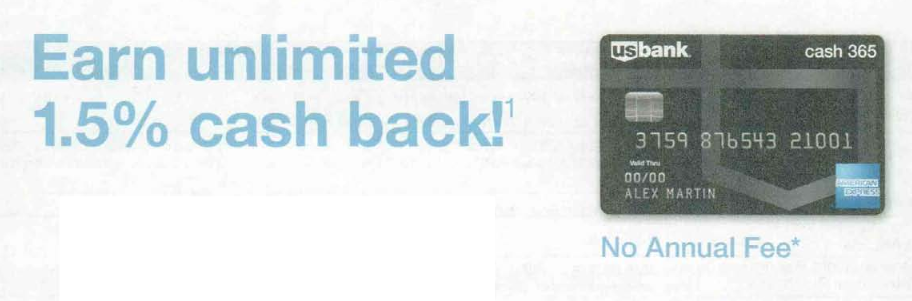

- U.S. Bank also offers another cashback card, the Cash 365 American Express card, which comes with the same unlimited 1.5% back on all purchases. The headline on the card landing page reads, “It’s simple. Your purchases equal cash back.” And a recent DM package leads with the idea of “unlimited” earn.

- USAA offers the Limitless Cashback Rewards Visa Signature card with 2.5% back. There is a “catch” here, but it’s not a cap (the card is called “limitless” after all). Cardholders need to maintain a $1,000 direct deposit in a USAA checking account. Since USAA targets its current members with product offerings, this cross-sell play could work better for this brand than it might for other issuers.

- Last year, Wells Fargo debuted its Cash Wise Visa Signature card that offers unlimited 1.5% back. One of the benefits the marketing touts? “No category restrictions or quarterly sign-ups to limit cash rewards earnings.”

- Barclaycard has a CashForward World MasterCard with an unlimited 1.5% back and a 5% redemption bonus.

- The lead card product on PenFed’s website is this Power Cash Rewards Visa Signature

There are two earn options for this card, but they are different offers, not tiers. With the first offer, cardholders get 1.5% back on all purchases. With the second, customers who have a PenFed checking account or are former members of the military get 2% back. The credit union leads with the idea of cash back on “Everything. Everywhere.” However, the first supporting benefit listed is “Rewards are unlimited!”

Complex and distinct vs. simple and straightforward

Almost every issuer offers a cashback card, so this is a very crowded product space. It’s not surprising to see tension between two main approaches:

- the more complex value proposition that can be positioned and marketed in a distinct way

vs.

- the simple, back to basics flat earn with straightforward messaging that focuses on “unlimited.”

What’s interesting for us as marketers is that the more recently launched products seem to be of the latter – flat earns with no caps. This suggests that issuers are trying to respond to consumer insights about cashback cards and pulling back from the tiered earn.

In our experience, it’s generally true that simpler is better, especially with cashback cards. Complex value propositions can feel like work to consumers, and while financial marketers understand how they work, consumers generally crave a straightforward approach they don’t have to think about.